You’ve probably heard about the 50/30/20 rule floating around personal finance circles. Spend 50% on needs, 30% on wants, 20% on savings. Sounds neat and tidy, right? But when your HDB flat costs a fortune, hawker meals keep creeping up, and everyone around you seems to be eating at fancy restaurants, you start wondering if this American budgeting framework even makes sense for Singaporeans.

The 50/30/20 rule allocates 50% of your income to needs, 30% to wants, and 20% to savings. While it works as a starting framework for young Singaporeans, high housing costs and mandatory CPF contributions mean you’ll likely need to adjust the percentages. Most locals find success with a modified 60/20/20 or 55/25/20 split that accounts for Singapore’s unique cost structure.

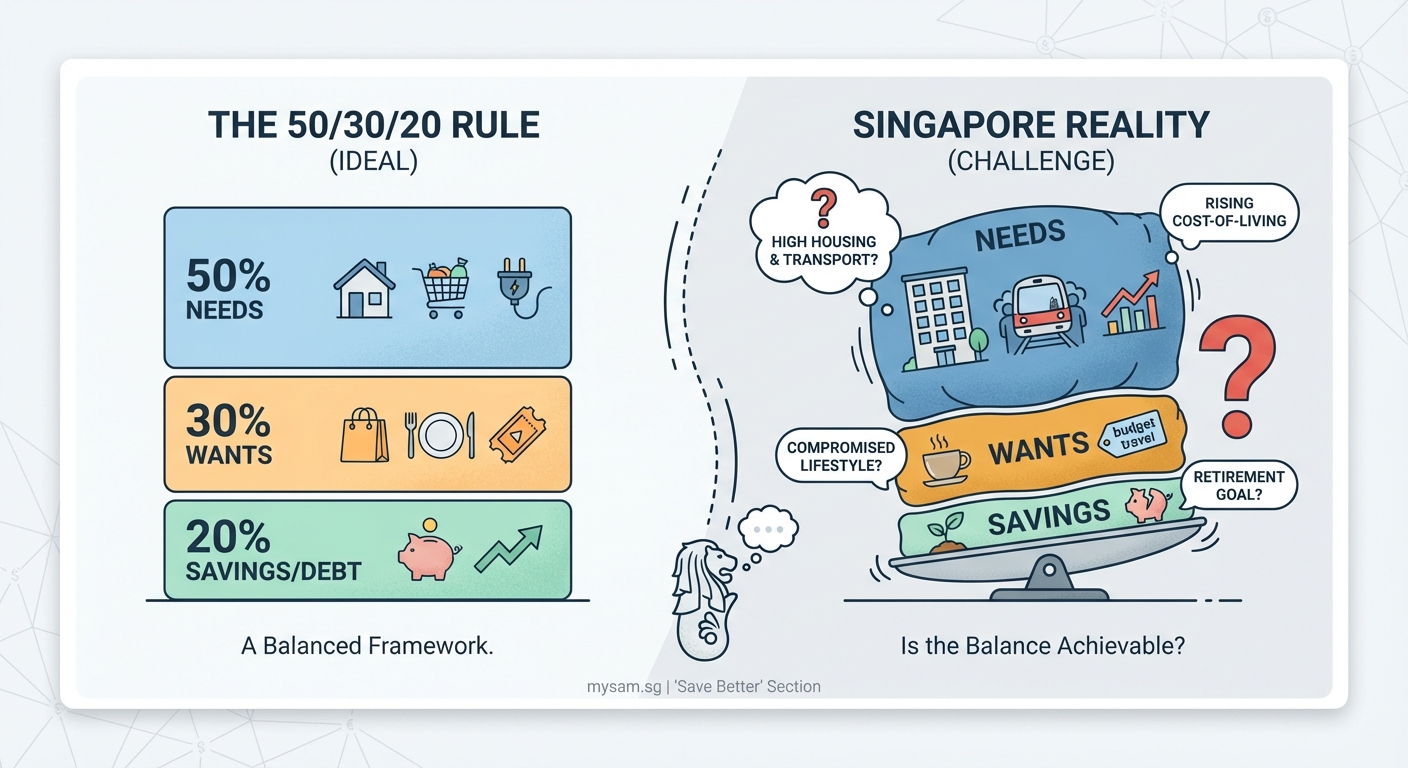

What is the 50/30/20 rule?

The 50/30/20 rule is a budgeting method created by U.S. Senator Elizabeth Warren. It breaks your after-tax income into three categories.

Needs (50%) cover essentials you can’t live without. Think rent, utilities, groceries, transport, insurance, and minimum loan payments.

Wants (30%) are the fun stuff. Dining out, Netflix subscriptions, new clothes, concerts, holidays, and that bubble tea habit.

Savings (20%) goes toward your future. Emergency funds, investments, extra debt payments, and retirement accounts.

The beauty of this rule is its simplicity. You don’t need a complicated spreadsheet. Just three buckets.

But here’s the catch. This framework was designed for Americans with very different living costs and no mandatory retirement savings like our CPF.

How Singapore’s reality changes the math

Singapore throws a few curveballs at the standard 50/30/20 split.

CPF contributions eat into your take-home pay. If you’re earning $4,000 monthly, your employer contributes 17% and you contribute 20% to CPF. That’s $1,480 going straight to CPF before you see a cent. Your actual take-home is $3,200, not $4,000.

Housing costs are brutal. A typical HDB flat mortgage can easily consume 30-40% of your take-home pay, even with CPF contributions. Add utilities, internet, and property tax, and your “needs” category is already bursting.

Transport isn’t cheap. Even if you take public transport everywhere, monthly passes add up. Own a car? You’re looking at $1,000+ monthly just for loans, insurance, petrol, and parking.

Healthcare and insurance matter more. While we have Medisave, you still need to budget for private insurance riders, dental care, and other health expenses that CPF doesn’t cover.

These factors mean sticking to the traditional 50/30/20 split becomes nearly impossible for most young professionals here.

Breaking down the 50/30/20 rule for Singapore salaries

Let’s run through some real numbers. Say you’re 28, earning $4,500 gross monthly. After CPF deductions, you take home $3,600.

Standard 50/30/20 allocation

| Category | Percentage | Monthly Amount |

|---|---|---|

| Needs | 50% | $1,800 |

| Wants | 30% | $1,080 |

| Savings | 20% | $720 |

Now let’s see if this actually works with typical Singapore expenses:

Needs ($1,800 budget):

– HDB loan (3-room, after CPF): $400

– Utilities and internet: $150

– Groceries: $400

– Transport: $120

– Insurance (term life, health riders): $200

– Phone plan: $30

– Parents’ allowance: $300

– Total: $1,600

You’re within budget, but just barely. And this assumes you’re not paying for a car, don’t have student loans, and split housing costs with a partner or family.

Wants ($1,080 budget):

– Dining out (8 times): $400

– Streaming services: $40

– Gym membership: $80

– Shopping and personal care: $200

– Entertainment and hobbies: $150

– Occasional trips: $210

– Total: $1,080

This works, but you need discipline. One extra staycation or wedding dinner can blow the budget.

Savings ($720):

This goes into your emergency fund first, then investments. Since CPF already handles retirement basics, this $720 can focus on building wealth outside the system.

At first glance, the 50/30/20 rule seems doable. But most Singaporeans find the “needs” category quickly balloons beyond 50%.

When the 50/30/20 rule breaks down in Singapore

The framework starts cracking under pressure in several common scenarios.

You’re living alone. Rent for a studio or room easily hits $1,000-$1,500. Suddenly your needs category jumps to 60-70% of take-home pay.

You have a car. Add $1,200 monthly for car expenses and your needs shoot past 65%. The 50% allocation becomes fantasy.

You’re supporting parents or family. Many young Singaporeans give $500-$800 monthly to parents. That’s another 15-25% of a typical salary.

You’re paying off student loans. Private university graduates might have $300-$500 monthly loan payments on top of everything else.

You work in a role requiring appearance upkeep. Some jobs expect you to dress well, maintain a certain look, or entertain clients. These “professional wants” blur into needs.

In these situations, trying to force the 50/30/20 split creates stress rather than clarity.

Modified budgeting ratios that work better here

Most financial advisors in Singapore recommend adjusting the percentages to match local realities.

The 60/20/20 split

Allocate 60% to needs, 20% to wants, 20% to savings. This acknowledges that housing and transport simply cost more here.

The 55/25/20 split

A middle ground that gives you slightly more breathing room for both needs and wants while maintaining the same savings rate.

The 50/20/30 split (flipped)

Some people flip wants and savings, prioritizing building wealth over lifestyle spending. This works well if you’re naturally frugal or have specific financial goals.

“The best budget is the one you’ll actually follow. If the traditional 50/30/20 makes you feel like you’re constantly failing, adjust the percentages to fit your reality. The principle matters more than the exact numbers.”

The key is maintaining that 20% minimum for savings while being honest about what truly counts as a need versus a want.

Step-by-step guide to applying the rule in Singapore

Ready to try this framework? Here’s how to adapt it for your situation.

-

Calculate your true take-home pay. Start with your gross salary, subtract CPF contributions, and that’s your working number. Don’t use gross income or you’ll set yourself up for failure.

-

Track one month of actual spending. Use a budgeting app or simple spreadsheet to record every expense for 30 days. No judgment, just data collection.

-

Categorize ruthlessly. Go through each expense and mark it as need, want, or savings. Be honest. That daily Starbucks is a want, not a need.

-

Calculate your current percentages. Add up each category and divide by your take-home pay. You might be shocked to find you’re spending 70% on needs and only saving 5%.

-

Identify your biggest gaps. If needs are eating 65% of income, look for ways to trim. Can you refinance your loan? Cut grocery costs? Move closer to work?

-

Set realistic targets. Don’t jump from 5% savings to 20% overnight. Aim for 10% next month, then 15%, then 20%. Gradual change sticks.

-

Automate your savings. Set up automatic transfers on payday. If you’re aiming for 20% savings on $3,600 take-home, that’s $720 moving to a separate account before you can spend it.

-

Review and adjust monthly. Spending patterns change. Your budget should flex with them. Check in every month and tweak as needed.

Common mistakes Singaporeans make with this rule

Even with the best intentions, people trip up in predictable ways.

| Mistake | Why It Happens | How to Fix It |

|---|---|---|

| Treating CPF as “savings” in the 20% | CPF is retirement savings, but it’s locked up | Count CPF separately; your 20% should be liquid or invested |

| Miscategorizing wants as needs | “I need to eat out for work” becomes an excuse | If it’s truly work-required, your employer should cover it |

| Ignoring irregular expenses | Insurance premiums, car servicing, annual subscriptions | Create a “sinking fund” in your needs category for these |

| Setting unrealistic want percentages | Trying to live on 10% wants while everyone around you spends freely | Be honest about your lifestyle; cutting too deep leads to budget rebellion |

| Not accounting for inflation | Your budget from 2024 won’t work in 2026 | Review and increase allocations annually as costs rise |

The biggest trap? Comparing your budget to friends who might earn more, have family support, or are quietly drowning in debt.

Maximizing your savings and wants categories

Once you’ve got your needs under control, you can optimize the other two buckets.

For your 20% savings:

Start with an emergency fund covering six months of expenses. This is your financial airbag.

After that, begin investing even with small amounts. Time in the market beats timing the market.

Consider maxing out your SRS contributions for tax relief if you’re in a higher income bracket.

For your 30% wants:

Use cashback credit cards strategically to stretch your dining and entertainment budget further.

Look for free or cheap entertainment options. Singapore has tons of free museums, parks, and community events.

Practice the 24-hour rule. Wait a day before buying anything over $50. You’d be surprised how many “must-haves” lose their appeal.

What to do when the rule just doesn’t fit

Sometimes your income is too low or expenses too high for any percentage split to work comfortably.

Increase your income. This is often easier than cutting expenses to the bone. Consider negotiating a raise, picking up a side hustle, or even trying affiliate marketing.

Reduce your biggest expenses. For most people, that’s housing. Can you get a roommate? Move to a cheaper area? Refinance your loan?

Temporarily adjust your targets. If you’re dealing with a crisis or major life change, it’s okay to save 10% instead of 20% for a few months. Just make sure “temporary” doesn’t become permanent.

Focus on the gap, not the goal. If you’re currently saving nothing, getting to 5% is a massive win. Celebrate progress rather than beating yourself up for not hitting 20% immediately.

The rule is a tool, not a religion. If it’s not serving you, modify it or use a different framework entirely.

Making the numbers work for your situation

The 50/30/20 rule isn’t magic. It’s a starting point for thinking about money in three clear categories.

For most young Singaporeans, a modified version like 60/20/20 or 55/25/20 reflects reality better. The specific percentages matter less than the habit of intentionally allocating your income instead of wondering where it all went.

Start by tracking one month honestly. See where you actually stand. Then adjust the percentages to match your life while pushing yourself to save at least 15-20% if you possibly can.

Your budget will look different from your friends’ budgets. That’s not just okay, it’s expected. What matters is that you’re making conscious choices about your money rather than letting it slip away unnoticed.

The best time to start was last month. The second best time is right now.