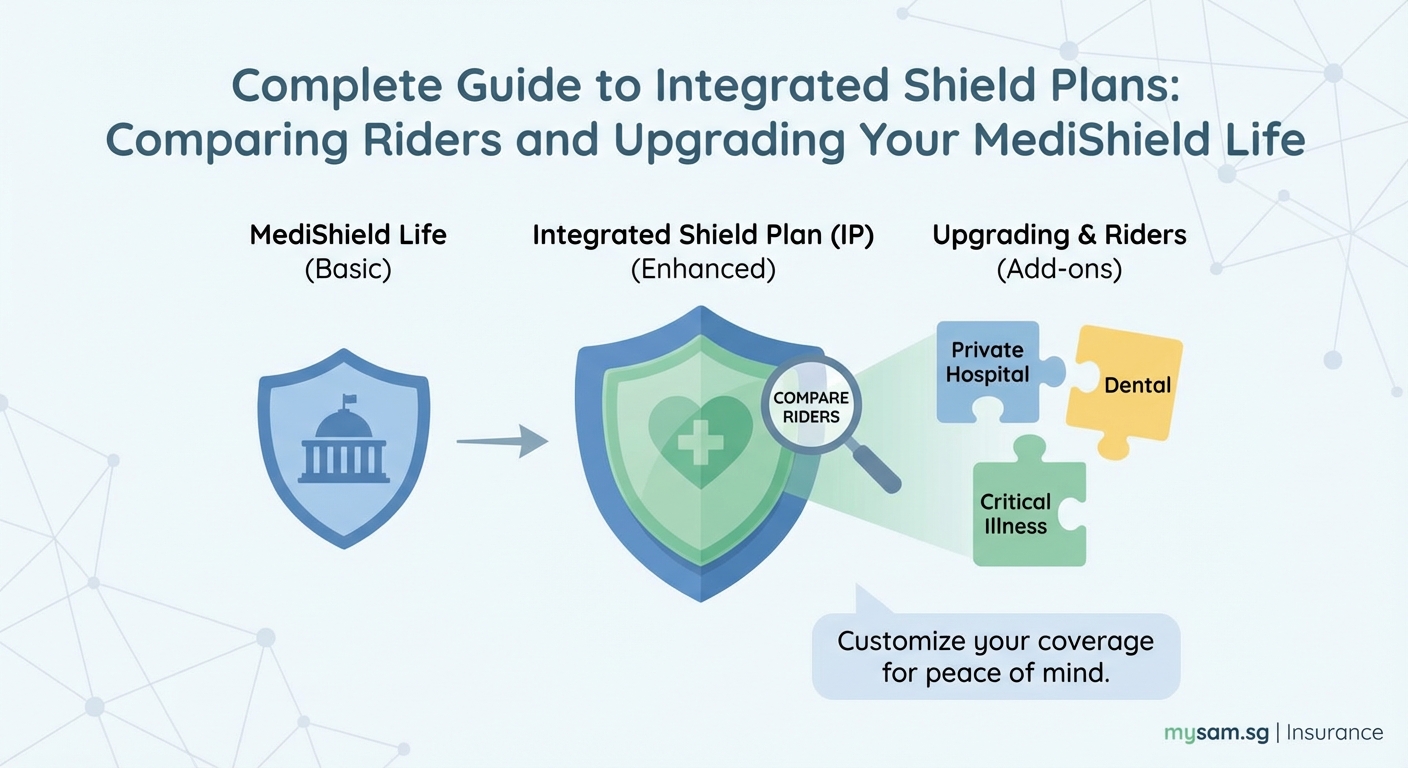

MediShield Life covers the basics, but a single hospital stay can still leave you with a hefty bill. That’s where Integrated Shield Plans come in. These private insurance policies work alongside your government coverage to protect you from unexpected medical costs that could wipe out your savings.

Integrated Shield Plans upgrade your MediShield Life coverage by paying for private or Class A ward stays. All seven insurers in Singapore offer similar base plans but differ in premiums, rider options, and claim processes. Most people add a rider to reduce out-of-pocket costs to zero or near zero. Your choice depends on your budget, preferred hospitals, and whether you want full coverage or are comfortable with some co-payment.

What are Integrated Shield Plans and how do they work

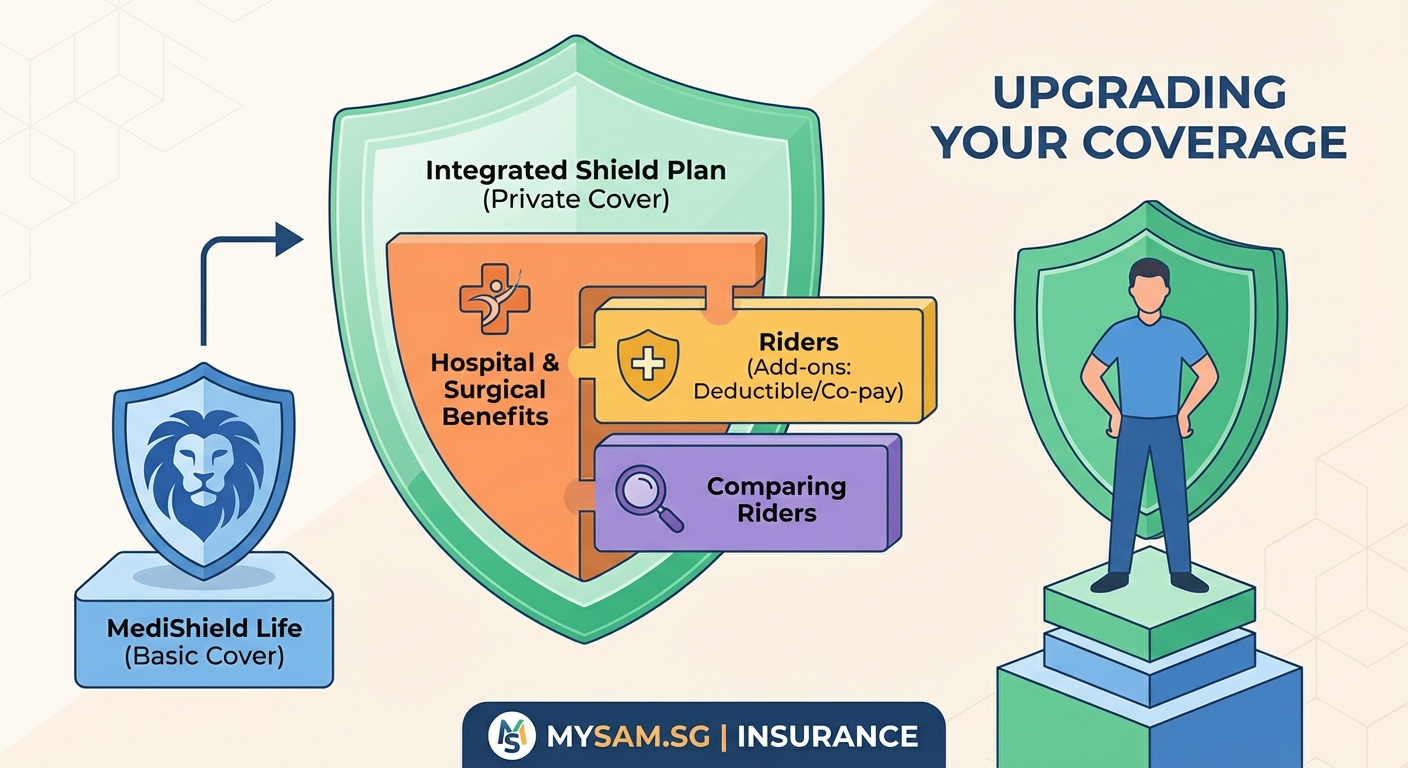

Integrated Shield Plans are private health insurance policies approved by the Ministry of Health. They build on top of MediShield Life, which only covers Class B2 and C wards in public hospitals.

Think of it this way. MediShield Life is your foundation. It pays part of your hospital bill if you stay in a government hospital ward. But the coverage stops there.

An Integrated Shield Plan extends that protection. It lets you stay in private hospitals or better wards without paying the full cost yourself.

Here’s what makes them special. You can use your CPF MediSave to pay for the premiums, up to certain limits. The government sets these limits each year based on your age.

Seven insurers offer these plans in Singapore:

* AIA HealthShield Gold Max

* AXA Shield

* Great Eastern GREAT SupremeHealth

* Income Enhanced IncomeShield

* NTUC Income Shield

* Prudential PRUShield

* Raffles Shield

All seven plans must meet government standards. They cover similar things like hospitalization, surgery, and some outpatient treatments after your hospital stay.

The base plan typically covers you for stays in a private hospital or Class A ward in a public hospital. You’ll still pay some costs out of pocket, called co-insurance and deductibles.

That’s where riders come in. A rider is an add-on that reduces or removes your out-of-pocket costs. More on that later.

Understanding the costs behind each plan

Premium is what you pay regularly to keep your coverage active. This amount increases as you get older because medical costs rise with age.

Let’s look at what a 30-year-old might pay annually for base coverage:

| Insurer | Approximate Annual Premium | Ward Coverage |

|---|---|---|

| AIA | $400 to $500 | Private hospital |

| AXA | $380 to $480 | Private hospital |

| Great Eastern | $420 to $520 | Private hospital |

| Income | $390 to $490 | Private hospital |

| Prudential | $410 to $510 | Private hospital |

| Raffles | $430 to $530 | Private hospital |

These numbers shift based on your exact age, gender, and smoking status. Women generally pay less than men. Smokers pay more.

You can pay using three methods:

1. CPF MediSave (up to withdrawal limits)

2. Cash or credit card

3. A combination of both

Most people max out their MediSave first, then top up the rest with cash.

Deductible is the amount you must pay before your insurance kicks in. For private hospital plans, this is typically $3,500 per year. If your bill is $20,000, you pay the first $3,500, and insurance covers the rest.

Co-insurance is the percentage you share with the insurer after the deductible. Standard co-insurance is 10%. Using the same example, after your $3,500 deductible, you’d pay 10% of the remaining $16,500, which is $1,650.

So your total out-of-pocket cost would be $5,150 for a $20,000 bill. That’s still significant for many families.

How riders reduce your hospital bills to almost nothing

A rider is optional coverage you add to your base plan. It covers most or all of your deductible and co-insurance amounts.

There are two main types.

Full riders cover 100% of your deductible and co-insurance. You pay nothing when you make a claim, except for non-claimable items like TV rental or extra meals.

These are the most expensive riders. They can cost an additional $300 to $600 per year for a 30-year-old.

Co-payment riders cover everything except a small fixed amount per claim. You might pay $500 or $1,500 out of pocket, and the rider handles the rest.

These cost less, around $150 to $400 annually for a 30-year-old.

“Most Singaporeans choose a rider because hospital bills can easily hit $30,000 or more for serious conditions. Without a rider, you’re looking at $5,000 to $6,000 out of pocket even with base coverage. That’s a lot for most families to handle without stress.”

The catch is that riders cannot be paid using MediSave. You must use cash.

Here’s a practical scenario. You’re 35 and need surgery. The bill comes to $40,000.

Without a rider:

* Deductible: $3,500

* Co-insurance (10% of $36,500): $3,650

* Total you pay: $7,150

With a full rider:

* Total you pay: $0 (except non-claimable items)

With a co-payment rider ($1,500 co-payment):

* Total you pay: $1,500

The rider makes a huge difference in protecting your savings.

Comparing the seven insurers side by side

All seven insurers offer similar coverage because they must follow government guidelines. But they differ in three key areas.

Premium pricing

Some insurers charge more than others for the same level of coverage. The difference can be $100 to $200 per year when you’re young, but it widens as you age.

Claim process

Some insurers have faster approval times and simpler paperwork. Others require more documentation or take longer to process claims.

Income and AIA are known for smoother claim experiences based on customer feedback. Prudential and Great Eastern also have strong reputations.

Panel hospitals

Most insurers work with all private hospitals in Singapore. But some have preferred partnerships that might give you better service or faster approvals.

Check which hospitals are on your insurer’s panel. If you have a preferred doctor or hospital, make sure your plan covers it fully.

Additional benefits

Some plans include extras like:

* Annual health screenings

* Dental coverage for accidents

* Traditional Chinese Medicine treatments

* Mental health support

These vary by insurer and plan tier.

Here’s a comparison of what matters most:

| Feature | What to Check | Why It Matters |

|---|---|---|

| Premium at age 30 | Starting cost | Affects your budget now |

| Premium at age 60 | Future cost | Affects retirement planning |

| Claim settlement ratio | Percentage of claims approved | Shows reliability |

| Panel hospitals | List of covered facilities | Ensures your preferred hospital is included |

| Rider options | Types and costs | Determines your out-of-pocket maximum |

Choosing between plan tiers and coverage levels

Most insurers offer multiple tiers. Higher tiers cover better wards or hospitals.

Standard private hospital plans cover any private hospital or Class A ward in public hospitals.

Some insurers offer plans for Class B1 wards only. These cost less but limit where you can stay.

There are also plans for single-bedded wards in private hospitals. These cost more but give you a private room.

Your choice depends on three factors:

Your budget

Can you afford higher premiums now and in the future? Remember, premiums increase with age.

A 30-year-old might pay $400 annually. By 60, that could jump to $2,500 or more for the same plan.

Your healthcare preferences

Do you want to see private specialists? Stay in a private room? Have more control over your treatment schedule?

Private hospitals offer more comfort and convenience. Public hospitals provide excellent care but with longer wait times and shared wards.

Your existing savings

If you have substantial emergency savings, you might skip the rider and handle co-payments yourself. This saves on premiums.

If your emergency fund is limited, a rider protects you from unexpected large bills.

Most people in their 30s and 40s choose a standard private hospital plan with a co-payment rider. This balances cost and protection.

Steps to upgrade from MediShield Life

Ready to get an Integrated Shield Plan? Here’s how to do it.

-

Compare premiums across all seven insurers. Use online comparison tools or visit each insurer’s website. Get quotes for your exact age and circumstances.

-

Decide on your coverage level. Choose between private hospital, Class A, or Class B1 coverage. Consider your budget and preferences.

-

Choose whether to add a rider. Calculate what you’d pay out of pocket without a rider. Compare that to the annual rider cost.

-

Check pre-existing conditions. Insurers may exclude coverage for conditions you already have. Be honest in your application to avoid claim rejections later.

-

Submit your application online or through an agent. You’ll need your NRIC, CPF information, and medical history.

-

Complete any required medical checks. Some applicants need health screenings, especially if you’re older or have health issues.

-

Set up your payment method. Link your MediSave for automatic deductions. Add a credit card for any amounts exceeding MediSave limits.

The whole process takes one to three weeks. You’ll receive a policy document once approved.

Common mistakes people make when comparing plans

Many people focus only on the cheapest premium. But the lowest price today might not stay lowest as you age.

Some insurers increase premiums more aggressively than others. Check the premium schedule for your age group over the next 20 to 30 years.

Another mistake is not reading the fine print on exclusions. Pre-existing conditions, certain treatments, and experimental procedures might not be covered.

Here are the top errors to avoid:

- Choosing coverage based on current health without considering future needs

- Not factoring in premium increases over time

- Skipping the rider to save money, then facing large bills later

- Not checking if your preferred hospital or doctor is covered

- Forgetting that riders must be paid in cash, not MediSave

- Not reviewing your plan every few years as your situation changes

Some people also wait too long to get coverage. Premiums increase with age. A plan that costs $400 at age 30 might cost $600 at age 40 for the same coverage.

Apply when you’re young and healthy. You’ll lock in lower premiums and avoid potential exclusions for health conditions that develop later.

When to review and switch your plan

Your Integrated Shield Plan isn’t set in stone. You can switch insurers or adjust your coverage level.

Review your plan every three to five years, or when major life changes happen:

- Getting married or having children

- Changing jobs or income levels

- Developing new health conditions

- Approaching retirement

Switching insurers is allowed, but there are considerations. Your new insurer might impose fresh waiting periods or exclude new pre-existing conditions.

If you’ve stayed healthy and haven’t made claims, switching might get you better premiums. If you’ve developed health issues, staying with your current insurer is usually better.

You can also downgrade from a private hospital plan to a Class B1 plan to save money. This makes sense if your financial situation changes or you’re comfortable with public hospital care.

Upgrading is possible too, but the new insurer will assess your current health. Any conditions you’ve developed might be excluded.

Most people switch for two reasons: significantly lower premiums elsewhere, or better service and claim experience.

Before switching, compare the total cost including riders, check the new insurer’s claim reputation, and confirm your preferred hospitals are covered.

Making the right choice for your situation

There’s no single best Integrated Shield Plan for everyone. Your ideal choice depends on your personal circumstances.

If you’re young, healthy, and budget-conscious, consider a Class B1 plan or a private hospital plan without a rider. Build your emergency fund to handle potential out-of-pocket costs.

If you have a family or prefer certainty, a private hospital plan with a co-payment rider offers strong protection without breaking the bank.

If you want complete peace of mind and can afford it, a full rider eliminates all out-of-pocket costs.

The integrated shield plan comparison singapore landscape gives you options. Seven insurers compete for your business, which keeps prices relatively reasonable.

Take your time with this decision. Read the policy documents. Ask questions. Calculate the total cost over five to ten years, not just the current premium.

Your health coverage is one of the most important financial decisions you’ll make. Get it right, and you’ll sleep better knowing a medical emergency won’t destroy your finances. Choose a plan that fits your budget today while protecting your family tomorrow.