Your colleague just had twins. Another friend got divorced. Your neighbor sold their HDB and upgraded to a condo. Each of these moments should trigger an insurance review, but most people wait until something goes wrong before checking if their coverage still fits.

Insurance isn’t a set-it-and-forget-it purchase. Your life shifts constantly, and your policies need to keep pace. Reviewing at the right moments protects your family and your wallet.

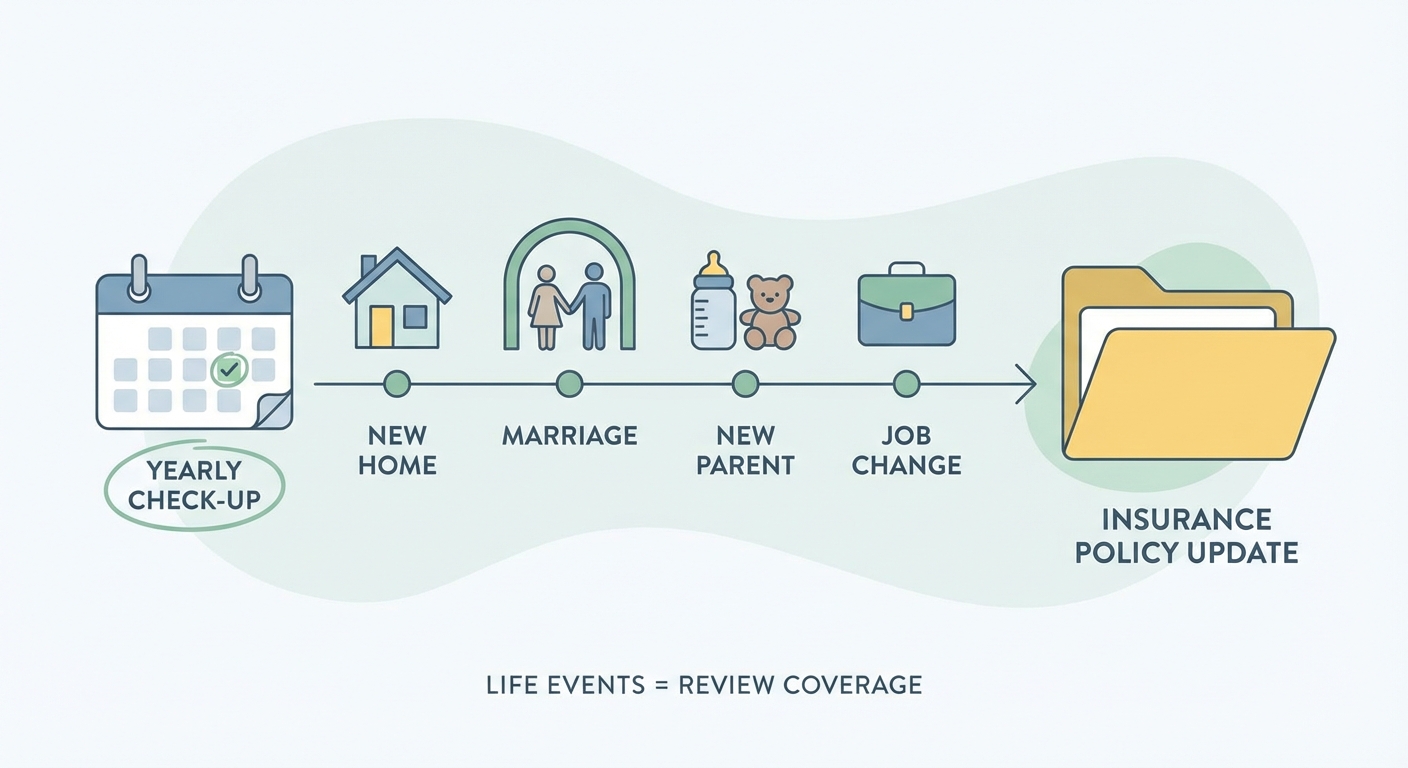

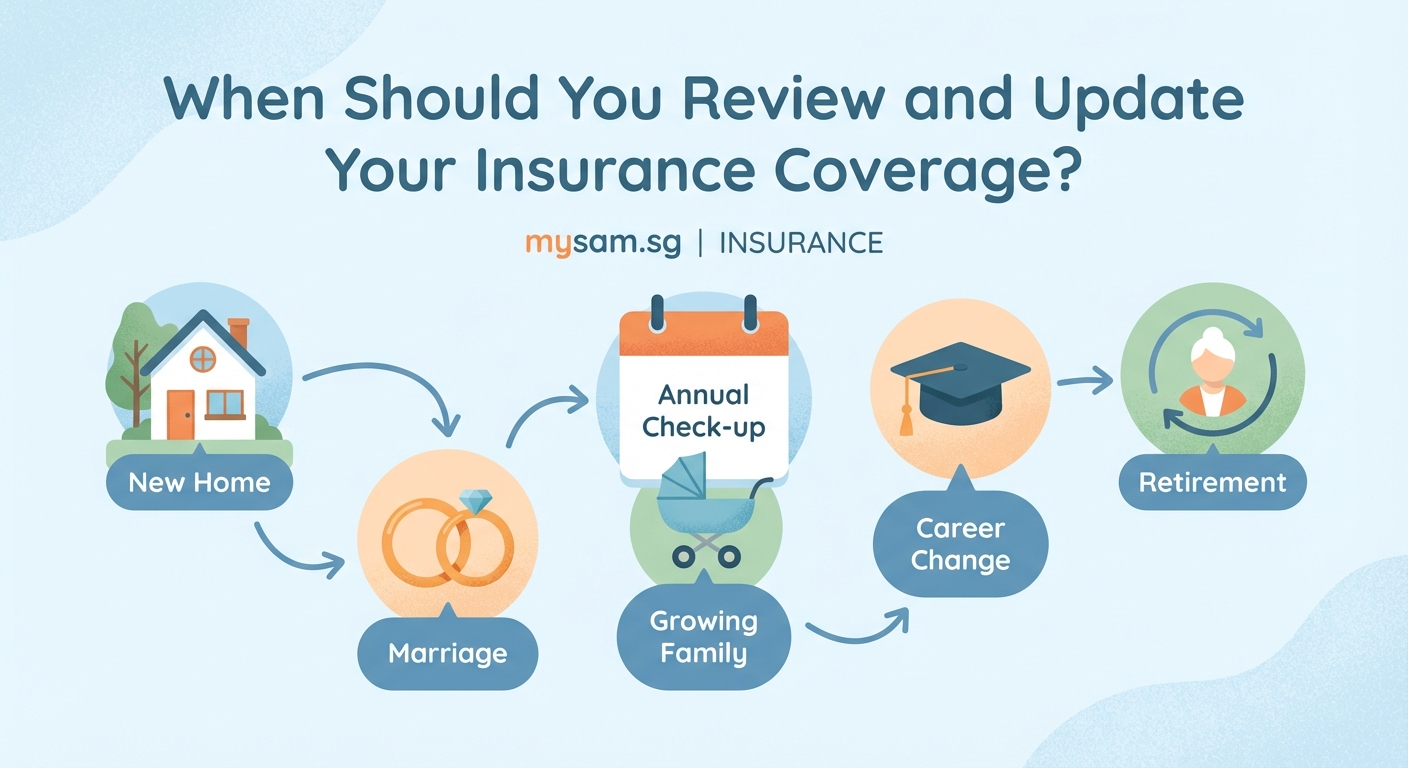

Review your insurance coverage during major life events like marriage, childbirth, property purchase, or career changes. Schedule annual check-ins every January to catch gaps before they become problems. Update beneficiaries immediately after any family change. Compare policies every three to five years to ensure you’re not overpaying for outdated coverage that no longer matches your needs.

Life events that demand an immediate review

Certain moments change everything about your insurance needs. Waiting even a few months can leave you exposed.

Getting married combines two financial lives. Your spouse now depends on your income. You might be taking on their debts or supporting their aging parents. Term life coverage that seemed adequate when you were single probably won’t cut it anymore.

Having a child multiplies your responsibilities overnight. You need enough coverage to replace your income until that child reaches adulthood. Calculate childcare costs, education expenses, and daily living needs for at least 20 years. Most new parents discover they’re underinsured by hundreds of thousands of dollars.

Buying property requires adjusting multiple policies. Your home loan needs mortgage reducing term assurance. Your contents need updating if you’ve upgraded furniture. Condo living brings different liability risks than HDB flats. Landed property owners face even more exposure.

Changing jobs can disrupt your group insurance. Some employers provide generous coverage that disappears the day you resign. Others offer minimal protection. Check what you’re losing and what you’re gaining before you sign that new contract.

Starting a business shifts you from employee to entrepreneur. You lose group coverage entirely. Your income becomes less predictable. You might need critical illness coverage that pays out faster or disability insurance that covers business expenses.

Divorce requires splitting policies and updating beneficiaries. Your ex-spouse might still be listed on your life insurance. Joint policies need separating. Child support obligations might require maintaining specific coverage amounts.

“I see clients every month who discover their ex-spouse is still the beneficiary on a $500,000 policy. They remarried years ago but never updated the paperwork. That’s a painful conversation for the new family.” (Insurance advisor, 15 years experience)

Annual reviews catch what life events miss

Even without major changes, your insurance needs drift over time. Set a specific date each year to review everything.

January works well for most people. You’ve just finished holiday spending and can see your actual financial picture. Tax season hasn’t started yet. Your mind is fresh.

During your annual review, check these specific items:

- Coverage amounts: Does your term life still replace 10 times your annual income?

- Premium costs: Have any policies increased significantly?

- Beneficiary details: Are names, IC numbers, and percentages still correct?

- Policy exclusions: Do you now have pre-existing conditions that affect claims?

- Riders and add-ons: Are you paying for benefits you never use?

Pull out every policy document. Create a simple spreadsheet listing the insurer, coverage amount, monthly premium, and renewal date. This takes about an hour but reveals gaps immediately.

Many Singaporeans discover they have three different hospitalization plans that overlap. Or they’re paying for personal accident coverage through their credit card, employer, and standalone policy. Consolidating saves money without reducing protection.

When your health status changes

Medical diagnoses trigger urgent insurance reviews, but you need to move carefully.

Before applying for new coverage, understand that most insurers ask about your medical history for the past five to ten years. A recent diagnosis might increase premiums or lead to exclusions. Sometimes keeping existing coverage beats trying to upgrade.

After a critical illness claim, your ability to get new coverage drops dramatically. Existing policies become more valuable. Check if your policy includes a retrenchment benefit or premium waiver that you haven’t activated.

During pregnancy, review hospitalization coverage for both mother and child. Some policies exclude pregnancy-related complications. Others require adding the newborn within 30 days of birth to avoid underwriting.

When chronic conditions develop, assess if your coverage handles long-term treatment. Diabetes, high blood pressure, and high cholesterol affect your insurability for decades. Locking in coverage before conditions worsen protects future options.

Property and vehicle milestones

Physical assets need coverage updates just like people do.

Renovating your home increases its value and your contents value. That $20,000 kitchen renovation isn’t covered unless you update your policy. Take photos of receipts and finished work.

Buying a car requires comparing comprehensive versus third-party coverage. New cars usually need comprehensive. Older cars might cost more to insure comprehensively than they’re worth.

Renting out property changes your home insurance requirements. Standard policies often exclude tenant-caused damage. Landlord insurance costs more but covers rental-specific risks.

Installing expensive items like solar panels, home gyms, or smart home systems requires notifying your insurer. These items increase your sum insured and might need separate coverage.

Career and income shifts

Your earning power determines how much coverage you need.

Salary increases should trigger coverage increases. If you earned $60,000 annually when you bought your policy and now earn $90,000, your family needs more protection to maintain their lifestyle.

Career changes affect risk profiles. Moving from an office job to construction work might increase premiums. Switching from employment to freelancing removes group coverage entirely.

Retrenchment makes some people want to cancel policies to save money. This is usually the worst time to drop coverage. Check if your policy includes premium waivers during unemployment.

Retirement lets you reduce some coverage. You might not need as much life insurance once your children are independent and your mortgage is paid. But you probably need more hospitalization coverage as medical needs increase.

Comparing your timing options

Different review schedules work for different situations. Here’s how they compare:

| Review Frequency | Best For | Advantages | Disadvantages |

|---|---|---|---|

| After every life event | Young families, entrepreneurs | Catches changes immediately | Can feel overwhelming |

| Annual review | Most working adults | Manageable routine | Might miss urgent gaps |

| Every 3-5 years | Retirees, stable situations | Low maintenance | Risk of outdated coverage |

| Policy renewal dates | Budget-focused buyers | Easy to remember | Spreads reviews across year |

Most people benefit from combining approaches. Review immediately after major life events, then schedule annual check-ins to catch everything else.

Red flags that mean review right now

Certain situations demand dropping everything and checking your coverage today.

Your insurer sends a renewal notice with a big premium jump. This happens when you age into a new bracket or when claims in your category increase. Compare quotes from other insurers before accepting the increase.

You receive a windfall. Inheritance, property sale profits, or business exits increase your net worth. Your existing coverage might not protect these new assets.

A family member gets seriously ill. Watching someone else struggle with medical bills or inadequate coverage often triggers your own review. Don’t wait for your own diagnosis.

You haven’t looked at your policies in five years. Insurance products improve constantly. Newer policies might offer better coverage for the same premium or similar coverage for less money.

Your children become financially independent. Once your kids can support themselves, you might not need as much life coverage. Redirect those premiums toward retirement savings or long-term care insurance.

Common mistakes during reviews

Even people who review regularly make these errors:

- Focusing only on price. The cheapest policy often has the most exclusions. Compare coverage details, not just premiums.

- Canceling old policies too quickly. Some older policies have better terms than current offerings. Check surrender values and benefits before canceling.

- Ignoring inflation. A $100,000 life policy bought in 2010 doesn’t have the same buying power in 2025. Increase coverage to match inflation.

- Forgetting about CPF nominations. Your CPF savings are separate from insurance but equally important for beneficiaries. Update both simultaneously.

- Not documenting changes. Keep written confirmation of every update. Insurers sometimes fail to process changes correctly.

Making your review process systematic

Turn insurance reviews from a dreaded chore into a simple routine.

- Create a master list of all policies with renewal dates, coverage amounts, and insurer contact details.

- Set calendar reminders three months before each renewal and one annual review date.

- Gather documents including recent payslips, property valuations, and medical records.

- Calculate your actual needs using online calculators or speaking with a fee-based advisor.

- Compare quotes from at least three insurers before making changes.

- Document everything including who you spoke with, what quotes you received, and why you made each decision.

This process takes about four hours annually but can save thousands of dollars and prevent devastating coverage gaps.

Keeping your coverage current without constant stress

Insurance reviews don’t need to consume your life. The goal is staying protected while you focus on actually living.

Set your annual review date now. Put it in your calendar with a reminder. When major life events happen, add a note to check your policies within the month.

Your insurance should work quietly in the background, ready when you need it but invisible when you don’t. Regular reviews keep it that way. You’ll sleep better knowing your family stays protected no matter what changes come next.