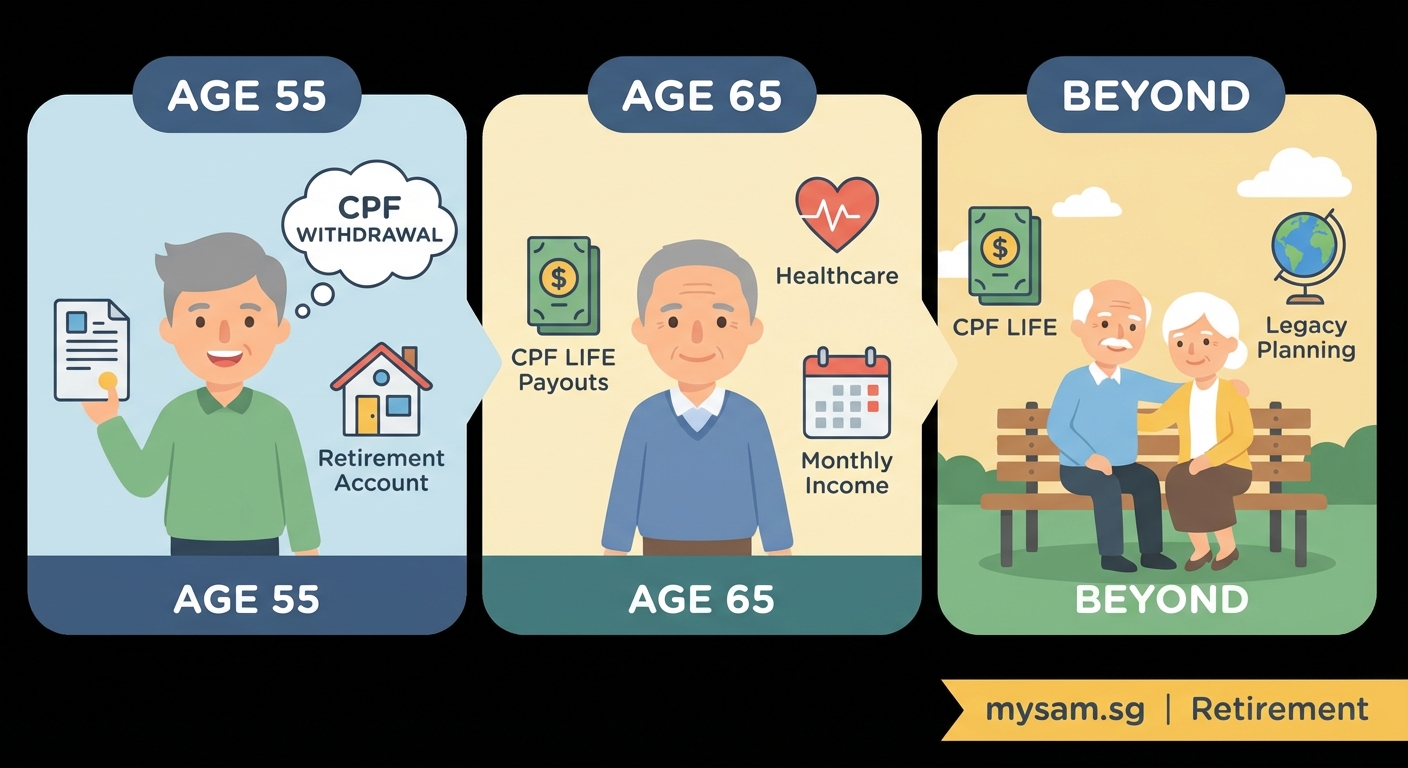

Turning 55 is a big deal for your CPF savings. It’s the age when your retirement accounts get reshuffled, withdrawal rules kick in, and you finally get access to some of your money.

But here’s the thing: most people don’t realize how complex the process actually is. The rules change at 55, then again at 65, and keep evolving as you age. Understanding what happens at each stage helps you plan better and avoid surprises.

When you turn 55, CPF creates your Retirement Account and sets aside money to meet your Basic Retirement Sum. You can withdraw any remaining savings above this amount. At 65, monthly CPF LIFE payouts begin. The amount you can access depends on your property status, retirement sums chosen, and total CPF balance at each milestone age.

The big shift at age 55

Your 55th birthday triggers an automatic restructuring of your CPF accounts. CPF will create a new Retirement Account (RA) by combining savings from your Special Account and Ordinary Account.

This isn’t just an administrative change. It determines how much you can withdraw immediately and how much gets locked away for retirement.

The system prioritizes setting aside enough money to fund your retirement years. Only after meeting this requirement can you access the excess.

How CPF calculates your Retirement Account

CPF moves money in a specific order:

- All your Special Account savings transfer to the new Retirement Account first

- If needed, money from your Ordinary Account tops up the RA to meet your retirement sum

- Any remaining balance stays in your Ordinary Account for withdrawal

The retirement sum amount changes every year. For 2024, the Full Retirement Sum stands at $205,800. This figure adjusts annually based on inflation and living costs.

Three retirement sum options

You get to choose between three levels, depending on your property ownership:

Basic Retirement Sum (BRS): Half of the Full Retirement Sum. You can only choose this if you own property with sufficient value pledged to CPF, or if your spouse pledges their property.

Full Retirement Sum (FRS): The standard amount. Most people without property pledges fall into this category.

Enhanced Retirement Sum (ERS): Three times the Basic Retirement Sum. This option gives you higher monthly payouts later but locks away more money now.

Your property situation matters here. If you own a home worth at least the BRS amount and pledge it, you free up more cash for immediate withdrawal.

What you can actually withdraw at 55

After CPF sets aside your chosen retirement sum, you can withdraw the excess. But the amount varies wildly between individuals.

Someone with $300,000 in total CPF savings choosing the Full Retirement Sum ($205,800) could withdraw about $94,200. Another person with only $150,000 would have nothing to withdraw if they don’t own property.

The withdrawal process happens in stages:

- Wait for CPF to send you a notification letter about one month before your birthday

- Log into your CPF account online after turning 55

- Submit a withdrawal application through the member portal

- Receive the money within five working days via bank transfer

You don’t have to withdraw everything at once. The money sits in your Ordinary Account earning interest until you need it.

Tax considerations for withdrawals

CPF withdrawals at 55 are not taxable as income. The money already belonged to you, so taking it out doesn’t create a tax liability.

However, if you use withdrawn CPF money for investments that generate returns, those investment gains may be taxable depending on the nature and scale of your activities.

Monthly payouts starting at 65

The money sitting in your Retirement Account isn’t just locked away. It’s working toward funding your CPF LIFE payouts, which begin at your payout eligibility age.

For most people born in 1958 or later, this age is 65. The exact age varies slightly for older cohorts.

CPF LIFE (Lifelong Income For the Elderly) is an annuity scheme. You receive monthly payments for as long as you live, protecting you from outliving your savings.

How payout amounts get determined

Your monthly payout depends on several factors:

- The total balance in your Retirement Account at your payout eligibility age

- The CPF LIFE plan you selected

- Prevailing interest rates and life expectancy projections

- Whether you deferred your payouts for higher amounts

The system offers three CPF LIFE plans:

| Plan | Monthly Payout | Bequest | Best For |

|---|---|---|---|

| Standard Plan | Moderate | Moderate | Balanced approach between income and legacy |

| Basic Plan | Lower | Higher | Those wanting to leave more to beneficiaries |

| Escalating Plan | Starts lower, increases | Lower | Those expecting to live longer or concerned about inflation |

Most members default into the Standard Plan unless they actively choose otherwise.

Deferring payouts for bigger checks

You can delay your CPF LIFE payouts up to age 70. Each year of deferral increases your monthly payment by roughly 7%.

This strategy works well if you’re still working past 65 or have other income sources. The higher payouts continue for life, so the longer you live, the more you benefit from deferring.

But deferring means no CPF LIFE income during those years. Make sure you have enough savings or income to cover expenses in the meantime.

Changes after 65 and beyond

Your CPF journey doesn’t freeze at 65. Several adjustments happen as you age further.

Voluntary contributions and top ups

After 55, you can still make voluntary contributions to your Retirement Account up to the current Full Retirement Sum.

These top ups enjoy tax relief up to $8,000 per year for contributions to your own account, and another $8,000 for contributions to family members’ accounts.

The money earns interest at Special Account rates (currently 4% per year) and increases your future monthly payouts.

“Top ups made before your payout starts will increase your monthly CPF LIFE payouts. Even small additional contributions compound over time and make a meaningful difference to retirement income.” — CPF Board

Healthcare account continues growing

Your MediSave Account remains separate throughout. It doesn’t merge into the Retirement Account and continues earning interest.

After 55, you can use MediSave for:

- Hospital bills and approved medical treatments

- MediShield Life premiums

- Approved outpatient treatments for chronic conditions

- Long term care insurance premiums

The Basic Healthcare Sum (BHS) applies here. Once your MediSave hits this amount (currently $71,500 for 2024), any excess can be withdrawn or used for family members’ medical expenses.

Property rules and your CPF

If you used CPF to buy property, the accrued interest continues accumulating even after 55. When you eventually sell the property, you must return this amount plus interest to your Retirement Account.

This can significantly impact your withdrawal calculations. Someone who used $200,000 in CPF for property decades ago might owe back $400,000 or more when selling, depending on how long the interest compounded.

Common mistakes people make

Understanding the rules is one thing. Avoiding costly errors is another.

Mistake 1: Withdrawing everything at 55

Many people treat their CPF withdrawal like a windfall and spend it immediately. This leaves them more dependent on CPF LIFE payouts alone during retirement.

Consider keeping some money in your Ordinary Account where it still earns interest. You can withdraw it anytime if emergencies arise.

Mistake 2: Ignoring the property pledge option

If you own property, pledging it to meet the Basic Retirement Sum frees up $102,900 more for withdrawal (half of the Full Retirement Sum).

Some people don’t realize they have this option and end up with less accessible cash than necessary.

Mistake 3: Not reviewing CPF LIFE plans

The default Standard Plan works for many people, but not everyone. If leaving an inheritance matters more than maximizing income, the Basic Plan might suit you better.

You can change your plan selection before payouts begin. After that, you’re locked in.

Mistake 4: Forgetting about nomination

CPF savings don’t automatically go through your will. Without a CPF nomination, the money gets distributed according to intestacy laws or through a lengthy claims process.

Making a nomination (which you can do online) ensures your savings go to your chosen beneficiaries smoothly.

Planning for each milestone

Smart CPF management means thinking ahead to each age milestone:

Before 55:

– Maximize contributions to hit higher retirement sums

– Consider voluntary top ups for tax relief and better payouts

– Decide whether to pledge property for more withdrawal flexibility

– Plan how you’ll use any withdrawal amounts

At 55:

– Review your retirement sum options carefully

– Don’t rush to withdraw everything

– Update your CPF nomination if life circumstances changed

– Calculate your expected CPF LIFE payouts

Between 55 and 65:

– Continue voluntary contributions if financially able

– Monitor your Retirement Account balance growth

– Decide whether to defer payouts past 65

– Review and switch CPF LIFE plans if needed

At 65 and beyond:

– Set up automatic transfers for your monthly payouts

– Keep MediSave topped up for healthcare needs

– Consider how property sales might affect your CPF

– Review beneficiary nominations periodically

Making the most of your CPF years

Your CPF savings represent decades of contributions. The rules at 55, 65, and beyond exist to balance immediate needs with long term security.

The key is understanding what happens at each stage so you can make informed choices. Whether that means withdrawing funds for a business venture, pledging property for more flexibility, or deferring payouts for higher income later, the decision should align with your overall retirement plan.

Take time to log into your CPF account and review your projections. The numbers tell a story about your retirement readiness. If the story doesn’t look quite right yet, you still have options to improve it through voluntary contributions, smart withdrawal timing, or adjusting your CPF LIFE plan selection.

Your 55th birthday opens new doors for your retirement savings. Walk through them with your eyes open and a clear plan in mind.