Insurance feels like one of those adult tasks that everyone puts off until something goes wrong. You know you need it, but between the jargon, the pushy agents, and the endless policy options, it’s easy to make mistakes that cost you thousands of dollars down the road.

Many Singaporeans end up either over-insured with policies they don’t need or dangerously under-covered when life throws a curveball. The good news? Most insurance mistakes are completely avoidable once you know what to watch out for.

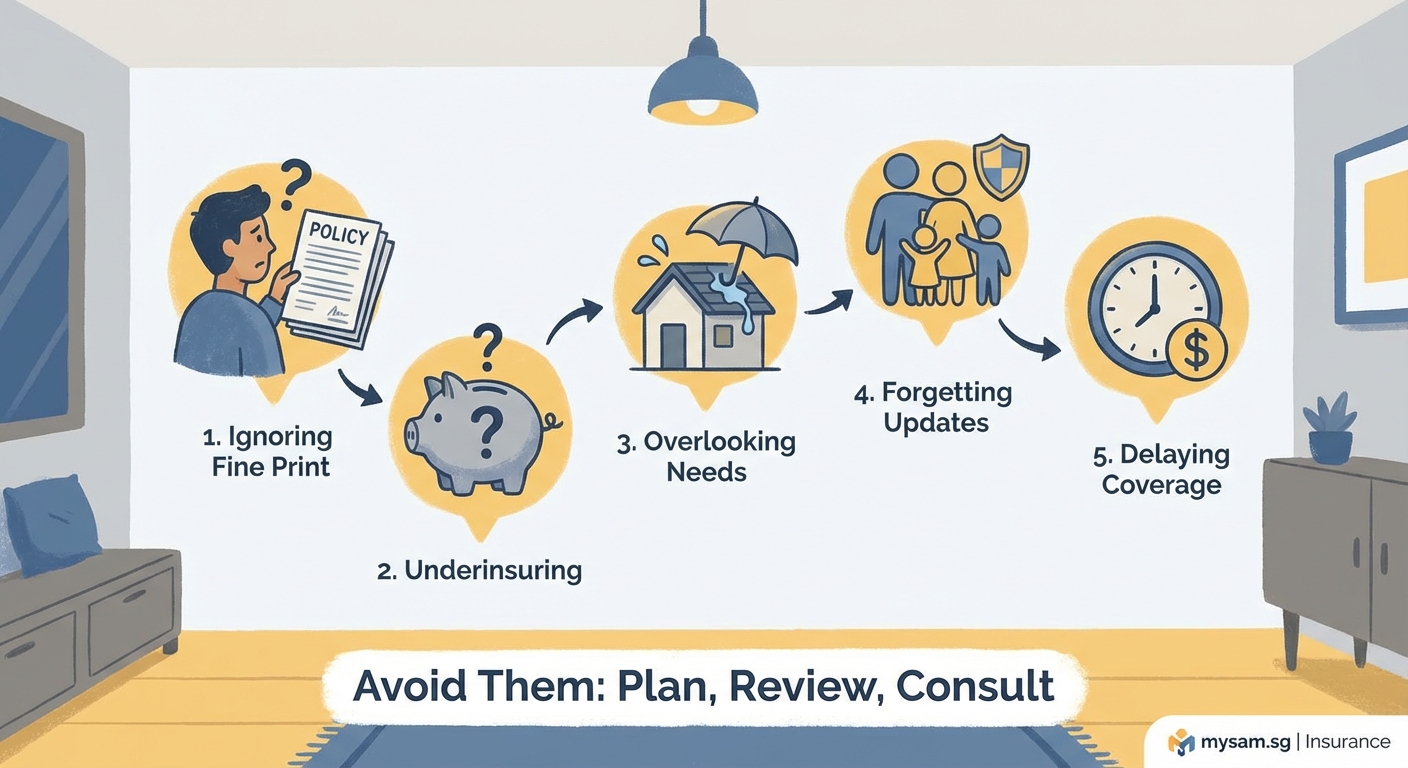

Singaporeans commonly make five major insurance errors: buying based on emotion rather than need, ignoring policy exclusions, failing to review coverage regularly, mixing investment with protection, and not comparing options. Understanding these mistakes helps you build smarter coverage that actually protects your finances without draining your wallet. This guide shows you exactly what to watch for and how to fix these issues before they become expensive problems.

Buying insurance based on emotion instead of actual needs

The insurance agent tells you a heartbreaking story about a family left with nothing after an unexpected death. You feel the weight of responsibility. Before you know it, you’ve signed up for a policy that costs $500 monthly and covers scenarios that don’t match your life.

This happens more often than you’d think.

Insurance companies train their agents to tap into your fears and emotions. While protection is genuinely important, your decisions should come from a clear assessment of your financial situation, not from anxiety or guilt.

Here’s how to avoid this trap:

- List your actual financial obligations before meeting any agent

- Calculate how much your dependents would need if you couldn’t work

- Factor in existing coverage from your employer or group policies

- Set a realistic budget based on your monthly cash flow

- Sleep on any decision for at least 48 hours before signing

A single 28-year-old renting a room and supporting no one needs vastly different coverage compared to a 38-year-old with two kids, a mortgage, and aging parents. Your policy should reflect your reality, not someone else’s sales target.

The best insurance plan is the one you can actually afford to maintain for the long term. A lapsed policy helps no one.

Ignoring the fine print and policy exclusions

You pay premiums faithfully for years. Then when you need to claim, you discover that your specific situation falls under an exclusion buried on page 47 of the policy document.

This scenario plays out daily in Singapore.

Policy exclusions aren’t there to trick you. They define the boundaries of what your insurer will and won’t cover. The problem is that most people never read them until it’s too late.

Common exclusions that catch Singaporeans off guard:

- Pre-existing conditions that weren’t disclosed during application

- High-risk activities like rock climbing or scuba diving

- Claims arising from alcohol or drug use

- Specific countries or regions excluded from travel coverage

- Waiting periods before certain benefits kick in

- Age limits that phase out coverage automatically

Before buying any policy, ask your agent to walk you through the exclusions section specifically. Don’t just nod along. Ask for real examples of what would and wouldn’t be covered.

If you already have policies, pull them out this weekend and actually read the exclusions. You might discover gaps that need addressing while you’re still healthy and insurable.

Treating insurance as an investment product

Walk into any bank in Singapore and someone will try to sell you an investment-linked policy (ILP) or whole life plan that promises both protection and returns. Sounds perfect, right?

The reality is messier.

These products combine insurance with investment components, which means they’re trying to do two jobs at once. Usually, they end up doing both poorly compared to buying term insurance and investing separately.

Here’s why the mix creates problems:

| Aspect | Combined Product | Separate Approach |

|---|---|---|

| Cost transparency | Hidden fees and charges | Clear premiums and investment fees |

| Flexibility | Locked in for decades | Can adjust coverage and investments independently |

| Returns | Often underwhelming after fees | Full control over investment choices |

| Coverage amount | Limited by premium budget | Maximum protection for lowest cost |

A 35-year-old paying $800 monthly for an ILP might get $200,000 coverage plus mediocre investment returns after fees. That same person could buy $500,000 of term coverage for $150 monthly and invest the remaining $650 in a diversified portfolio with lower fees and better potential returns.

The insurance industry makes significantly higher commissions on these combined products, which explains why agents push them so hard. Your financial interest and their sales incentive don’t always align.

If you want protection, buy pure protection. If you want investment returns, invest separately where you have full visibility and control.

Failing to review and update coverage regularly

You bought your first insurance policy at 25 when you landed your first job. Now you’re 35, married, with a child and a new condo. But your coverage still reflects your single, carefree days.

Life changes. Your insurance should change with it.

Most Singaporeans set up their policies once and forget about them until something goes wrong. That approach leaves dangerous gaps as your responsibilities grow.

Major life events that should trigger an insurance review:

- Getting married or divorced

- Having children or becoming a caregiver

- Buying property or taking on significant debt

- Starting a business or changing careers

- Reaching milestone ages (30, 40, 50)

- Changes to your health status

- Inheritance or significant wealth increase

Set a recurring calendar reminder every January to review all your policies. Check if your coverage amounts still make sense, if your beneficiaries are current, and if you’re paying for riders you no longer need.

Your employer coverage changes matter too. If you switch jobs and lose group insurance benefits, you need to fill that gap immediately. Don’t assume you’re still covered the same way.

Some policies become more expensive or less valuable as you age. A critical illness policy you bought at 30 might have premium increases at 40 that make it worth replacing with a better product.

Not comparing options before committing

Your colleague recommends her insurance agent. You meet once, the agent seems nice, and you sign up for whatever they suggest. You never check if better options exist.

This is how people end up paying 30% more than necessary for identical coverage.

Singapore has dozens of insurers offering similar products at vastly different prices. The agent who happens to contact you first might not represent the company with the best rates for your profile.

The comparison process doesn’t need to be overwhelming:

- Identify the specific type and amount of coverage you need

- Get quotes from at least three different insurers

- Compare not just premiums but also claim settlement ratios

- Check online reviews and complaints about each company

- Verify that the coverage terms are truly equivalent

| Factor | Why It Matters |

|---|---|

| Premium cost | Obvious impact on your monthly budget |

| Claim settlement ratio | Percentage of claims actually paid out |

| Exclusions | What situations aren’t covered |

| Riders available | Optional add-ons you might need later |

| Renewal terms | Can premiums increase? Under what conditions? |

| Financial strength | Will the insurer still exist in 30 years? |

Don’t feel obligated to buy from the first agent you meet just because they spent time with you. This is your money and your family’s protection. Shop around without guilt.

Online comparison tools can give you a starting point, but verify the details directly with insurers since these platforms sometimes show simplified versions that miss important differences.

Understanding the real cost of under-insurance

Some people try to save money by buying the bare minimum coverage or skipping insurance altogether. This strategy works perfectly until it doesn’t.

Medical bills in Singapore can easily hit six figures for serious conditions. A single hospital stay for cancer treatment might cost $150,000 or more after government subsidies. If your coverage caps at $50,000, you’re personally funding the gap.

Under-insurance shows up in several ways:

- Total coverage amount too low for your actual needs

- Hospitalization benefits that don’t match private hospital costs

- Income replacement that covers only 30% of your actual salary

- No coverage for critical illnesses that could sideline you for months

The math is straightforward. Saving $100 monthly on premiums feels good until you face a $200,000 medical bill that your policy only partially covers.

Calculate your actual exposure. Add up your debts, multiply your annual expenses by five years, factor in education costs for kids, and consider what your family would need if you couldn’t work. That’s your real coverage target.

Getting your coverage strategy right

Building proper insurance coverage doesn’t require a finance degree. It requires honesty about your situation and willingness to do basic homework.

Start with protection that addresses your biggest financial risks. For most working adults, that means adequate life and health coverage before anything else. Disability income protection matters more than most people realize since you’re statistically more likely to become unable to work than to die young.

Term life insurance gives you maximum coverage for minimum cost during your working years when dependents rely on your income. As you build wealth and your kids become independent, your need for life coverage naturally decreases.

Health insurance should be your foundation. MediShield Life covers basics, but integrated shield plans fill critical gaps for serious illnesses. Make sure your coverage matches where you’d actually seek treatment.

Avoid policies that try to do everything at once. Separate products for separate needs gives you flexibility and usually costs less overall.

Making insurance work for your actual life

Insurance mistakes cost Singaporean families millions in unnecessary premiums and uncovered claims every year. You don’t have to be part of that statistic.

Take an afternoon this month to review what you currently have. Pull out every policy document and check if the coverage still matches your life. Look for the gaps, the overlaps, and the products that made sense five years ago but don’t anymore.

Talk to your family about what would actually happen financially if something went wrong. Those conversations are uncomfortable but necessary. They tell you exactly what coverage you need and what you’re wasting money on.

The goal isn’t to buy the most insurance or the cheapest insurance. The goal is to buy the right insurance that actually protects your family without destroying your budget. That balance looks different for everyone, and it changes as your life changes.

Get it right, review it regularly, and you’ll sleep better knowing your family is genuinely protected.