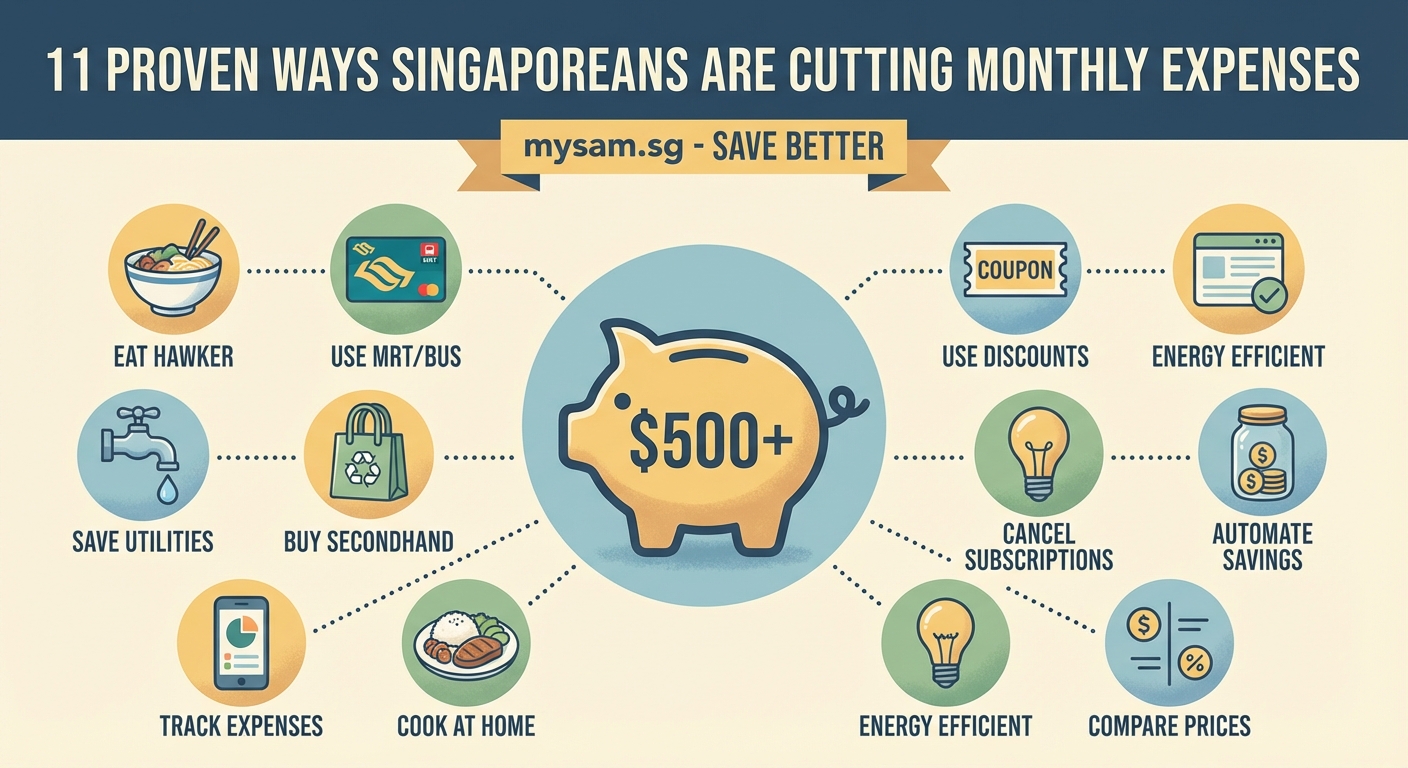

Rising costs hit differently when you see your bank balance shrink month after month. You’re earning decent money, but somehow it feels like there’s never enough left over at the end of the month. The good news? Hundreds of Singaporeans have figured out how to trim $500 or more from their monthly spending without giving up the lifestyle they enjoy.

Cutting monthly expenses in Singapore starts with tracking your spending patterns, then targeting high-impact categories like groceries, transport, and subscriptions. By switching to cashback cards, meal planning, and negotiating insurance premiums, middle-income households typically save between $500 to $800 monthly. The key is focusing on sustainable changes that fit your lifestyle rather than extreme deprivation that won’t last.

Why most expense-cutting advice doesn’t work

You’ve probably read articles that tell you to stop buying coffee or skip lunch with colleagues. That advice misses the point entirely.

Small daily purchases aren’t usually the problem. The real money drains are the monthly commitments you barely notice: insurance policies you never reviewed, gym memberships you forgot about, phone plans with data you never use.

The average Singaporean household spends between $4,500 to $6,000 monthly. Even a 10% reduction means an extra $450 to $600 staying in your account. That’s vacation money. Emergency fund money. Investment money.

Track your actual spending for 30 days

Before cutting anything, you need to know where your money goes. Not where you think it goes. Where it actually goes.

- Download a budgeting app or create a simple spreadsheet with these categories: housing, transport, food, insurance, utilities, subscriptions, entertainment, and miscellaneous.

- Record every single expense for one full month, including that $2.50 kopi and the $8 hawker lunch.

- At month’s end, calculate what percentage of your income goes to each category.

Most people get shocked during this exercise. You might discover you’re spending $400 monthly on food delivery when you thought it was maybe $150. Or that your “small” subscriptions add up to $120 monthly.

The numbers don’t lie. This tracking phase shows you exactly where to focus your cutting efforts.

Target the big three expense categories

Your spending likely follows the 80/20 rule: 80% of your money goes to 20% of your expense categories. Focus there first.

Housing costs

If you’re renting, this is often your biggest monthly expense. Here’s what works:

- Negotiate your lease renewal at least two months before expiry when landlords are more flexible

- Consider moving slightly further from the MRT if it saves you $300+ monthly

- Get a roommate if you’re renting a two-bedroom alone

For homeowners with mortgages, refinancing when interest rates drop can save $200 to $400 monthly on a typical HDB loan.

Transport expenses

Car ownership in Singapore costs an average of $1,200 to $1,800 monthly when you factor in loan payments, insurance, petrol, parking, and maintenance.

Switching to public transport plus occasional Grab rides typically costs $200 to $400 monthly. That’s a potential $1,000+ saving right there.

If giving up your car isn’t realistic, try these:

- Compare car insurance annually and switch providers if needed

- Use petrol credit cards that give 15% to 20% cashback at specific stations

- Carpool with colleagues who live nearby

- Work from home more often if your employer allows it

Food spending

The typical Singaporean spends $600 to $1,000 monthly on food. Cutting this by 30% saves $180 to $300 without eating instant noodles every day.

Meal planning makes the biggest difference. Decide your weekly meals on Sunday, buy ingredients in bulk at FairPrice or Sheng Siong, and cook larger portions that work for multiple meals.

“I used to spend about $850 monthly on food between hawker meals, cafes, and food delivery. After meal prepping just my weekday lunches and dinners, I’m down to $520. That’s $330 saved without feeling deprived because I still eat out on weekends.” – Sarah, 32, marketing manager

Cancel subscriptions you barely use

Pull up your credit card statements and highlight every recurring charge. You’ll probably find:

- Streaming services you signed up for one show and forgot about

- Gym memberships you haven’t used in months

- Cloud storage plans you don’t need

- Magazine or app subscriptions on auto-renew

Go through each one and ask: “Have I used this in the past 30 days?” If not, cancel it immediately.

The average person wastes $80 to $150 monthly on subscriptions they rarely use. That’s $960 to $1,800 yearly.

Switch to the right credit cards

Using the wrong credit card is like leaving money on the table every month.

Different cards excel at different spending categories. Build a simple two-card strategy:

| Spending Category | Best Card Type | Typical Cashback |

|---|---|---|

| Groceries | Supermarket cards | 5% to 10% |

| Petrol | Fuel-specific cards | 15% to 21% |

| Dining | Food cards | 8% to 10% |

| General spending | Cashback cards | 1.5% to 2% |

| Online shopping | E-commerce cards | 4% to 8% |

If you spend $800 monthly on groceries using a regular card with 0.5% cashback, you get $4 back. Switch to a card with 8% grocery cashback and you get $64 back. That’s an extra $60 monthly for literally zero effort.

Just pay off your balance in full every month. Credit card interest will destroy any cashback benefits.

Negotiate your insurance premiums

Most Singaporeans pay the same insurance premiums year after year without questioning them.

Call your insurance company before renewal and ask: “What discounts am I eligible for?” You’d be surprised how often they’ll lower your premium just for asking.

For car insurance, get quotes from at least three providers annually. Premiums can vary by $400 to $800 yearly for identical coverage.

For life and health insurance, review your policies every three years. Your needs change. That $500 monthly premium might include coverage you no longer need or duplicate coverage from your employer.

Working with an independent insurance advisor costs nothing and often finds you $100 to $200 in monthly savings by restructuring your policies properly.

Buy groceries strategically

Grocery shopping without a strategy wastes serious money.

- Never shop when hungry because you’ll buy 30% more than you need.

- Check FairPrice and Cold Storage apps for weekly promotions before heading out.

- Buy non-perishables in bulk when they’re on sale: rice, cooking oil, canned goods, toiletries.

- Choose house brands over name brands for items like pasta, flour, sugar, and cleaning supplies.

- Buy fruits and vegetables from wet markets instead of supermarkets for 20% to 40% savings.

One more thing: stop buying pre-cut vegetables and pre-marinated meats. You’re paying double for five minutes of convenience.

Reduce utility bills with simple changes

Aircon is the biggest electricity drain in Singaporean homes. Running it all night can cost $150 to $250 monthly.

Try these changes:

- Set temperature to 25°C instead of 22°C

- Use a timer to shut off after you fall asleep

- Service your aircon every three months so it runs efficiently

- Close bedroom doors to cool smaller spaces

Switching to LED bulbs saves $5 to $10 monthly. Not huge, but it adds up over a year.

For water bills, fix dripping taps immediately and take shorter showers. A leaking tap wastes about 20 liters daily, adding $10 to $15 to your monthly bill.

Cut entertainment costs without staying home

Entertainment doesn’t have to mean expensive. Singapore offers plenty of free or cheap options:

- Free museum entry for Singaporeans at National Gallery, National Museum, and Asian Civilisations Museum

- Community center classes at $5 to $15 per session

- Park connector cycling and hiking trails

- Free concerts at Botanic Gardens and Esplanade outdoor theater

- Library books, magazines, and e-books at zero cost

For paid entertainment, buy movie tickets on weekday mornings when they’re $8 instead of $14. Use aggregator apps for restaurant deals that give 20% to 50% off.

Set an entertainment budget of $150 to $200 monthly and stick to it. When it’s gone, switch to free activities.

Compare and switch service providers

Loyalty doesn’t pay when it comes to telco, broadband, and utilities.

Singapore’s deregulated market means you can switch providers easily. Mobile plans have gotten dramatically cheaper in recent years.

If you’re paying more than $30 monthly for your mobile plan, you’re probably overpaying. Most people need:

- 20GB to 50GB data

- Unlimited local calls and texts

- Basic roaming for occasional trips

Plans with these features now cost $15 to $25 monthly. Check Circles.Life, MyRepublic Mobile, GOMO, or Giga for better rates.

For broadband, compare plans annually. Providers constantly offer promotions for new customers. Switching every two years can save $20 to $40 monthly.

The same applies to electricity providers. Use the Open Electricity Market comparison tool and switch if you can save more than $10 monthly.

Common expense-cutting mistakes to avoid

| Mistake | Why It Fails | Better Approach |

|---|---|---|

| Cutting everything at once | Unsustainable and feels like punishment | Target three high-impact areas first |

| Choosing cheapest option always | Often costs more long-term | Focus on value, not just price |

| Not tracking results | Can’t see progress or adjust strategy | Review spending monthly |

| Ignoring small recurring charges | They compound to hundreds yearly | Audit subscriptions quarterly |

| Skipping insurance to save money | One emergency wipes out years of savings | Optimize coverage, don’t eliminate it |

The biggest mistake is treating expense-cutting as temporary. The changes that stick are the ones that become new habits, not short-term sacrifices.

Build your personalized cutting plan

Everyone’s financial situation differs. Your cutting plan should match your actual spending patterns and priorities.

Start with these steps:

- Review your 30-day spending tracking and identify your top five expense categories.

- Pick one strategy from this article for each of those five categories.

- Implement all five changes over the next 30 days.

- Track your total spending for the following month and calculate your savings.

- If you haven’t hit your $500 target, add two more strategies and repeat.

Most people who follow this approach save between $500 to $800 monthly within two months. Some save even more.

The key is consistency. Missing one month of tracking or letting old habits creep back in will undo your progress.

Make your money work harder for you

Cutting expenses is only half the equation. What you do with the money you save matters just as much.

Open a separate savings account and automatically transfer your monthly savings there. Treat it like a bill you must pay. This prevents lifestyle creep where your spending expands to fill whatever’s in your account.

Once you’ve built an emergency fund covering three to six months of expenses, consider putting your savings to work through:

- High-interest savings accounts earning 2% to 4% annually

- Singapore Savings Bonds for flexible, risk-free returns

- Robo-advisors for hands-off investing

- CPF top-ups for tax relief and guaranteed returns

The average Singaporean who cuts $600 monthly and invests it at 5% annual returns will have over $80,000 in ten years. That’s the power of redirecting wasted spending into wealth building.

Your next 30 days start now

You’ve just learned 11 proven strategies that hundreds of Singaporeans use to cut $500 or more from their monthly expenses. The question is: will you actually implement them?

Start today with the easiest win. Pull up your bank statement right now and cancel one subscription you don’t use. That takes three minutes and might save you $15 monthly.

Tomorrow, track every dollar you spend. Next week, compare your insurance and credit cards. By month’s end, you’ll have a clear picture of where your money goes and exactly how to keep more of it.

The financial pressure you’re feeling doesn’t have to be permanent. Small, strategic changes compound into significant savings that give you breathing room, build your emergency fund, and create real financial security.

Your $500 monthly savings journey starts with one decision today.